In the last edition of The Leonard Letter, Which Is Really More Risky?, we looked at risk from Person A and Person B.

For those who didn’t see the last edition, you can find it here.

Person A put 15% of their own cash into a deal and Person B put 0% of their own cash into their deal, but both ended up with the same amount of equity. I asked you to ponder, who really has more risk?

Now, I want to look at risk and down payment percentages from another perspective.

Please remember, this isn’t investing advice. This isn’t going to work for everyone’s situation, but this how I personally think about it.

I’m going to use round numbers here to make the illustration simple and easy to follow.

Let’s assume two people/couples have $65,000 in cash to buy a house and each couple chooses to buy a $312,500 house.

The first people put 20% down in cash ($62,500), so the loan balance is $250,000 and the monthly mortgage payment is about $1,000 (no insurance, taxes, or PMI considered).

Because they put such a high percentage down, they used up nearly all of the money they had saved and they won’t have much remaining ($2,500).

(Note: I know this isn’t a smart financial decision, but it’s very, very common)

The other people only put down 5% in cash ($15,625), so their loan balance is $296,875 and the monthly mortgage payment is about $1,250 (again, no insurance, taxes, or PMI considered).

Because they put a low percentage down, they have plenty of money left over to have as reserves, or to invest.

Murphy’s Law says anything that can wrong, will go wrong. Of course, this isn’t true in every scenario, but I’ve found it to be very true myself — whenever I buy a new property, something almost always goes wrong right away. Scott Trench, President and CEO of BiggerPockets, even talked about this on a recent podcast episode.

The first people have very little money to put aside for reserves in case something goes wrong. The second people have almost $50,000 they can put aside for reserves.

Sure, the second people are going to pay more interest over time, but who has more risk?

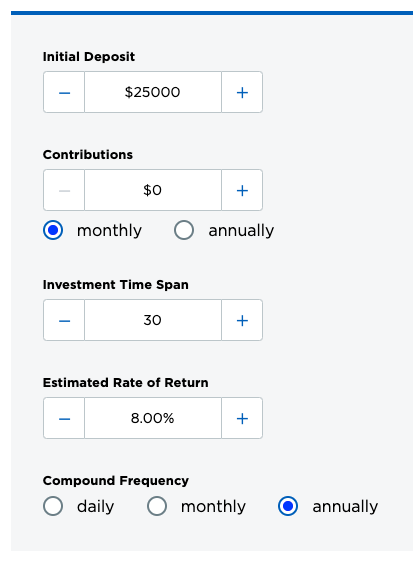

What if the second people invest $25,000 of their remaining $50,000 for the next 30 years? They’ll still have 10x the reserves of the first people, AND, at an 8% annual return, they’ll have over $250,000 just from that initial $25,000 investment (with no additional contributions).

I want to take this even one step further. The reality of people leaving that money invested for 30 years is low, and it’s possible nothing will go wrong with the property itself, so I want to look at it from another angle.

The first couple has a mortgage of $1,000 per month and $2,500 leftover after their down payment, right? So, that would mean, they have 2.5 months of their mortgage payment set aside. Assuming nothing with the property goes wrong, they would be able to pay their mortgage for 2.5 months with the amount of money they have leftover. Is that enough of an emergency fund to feel secure? If you lost your job or source of income, would 2.5 months be enough for you to feel secure?

The second couple has a higher mortgage payment of $1,250 per month, but they have 40 months of mortgage payments leftover! Would that make you feel secure? Let’s say they invest half of it as we discussed above. They would still have 20 months of mortgage payments leftover, AND they’d earn over $250,000 from their investments.

A lot of people see the higher monthly mortgage payment and automatically think it’s riskier.

But I challenge you to think about the above situations we just went over.

Who do you think truly has more risk?

This is how I personally approach real estate.

All the best,

Sponsored By

Norwood Energy drills and operates, profitably, oil & gas wells with a 90% success rate. A disciplined and economically-efficient approach provides investors the opportunity to benefit from a lower price point than most industry-level deals.

Hear more about Norwood Energy’s business here, or contact them directly at (817) 600-4246.

outstanding article