House hacking a $998k duplex in Oakland

Do the numbers pencil out?

Happy Friday! Today, we're diving into the numbers for a duplex on the market in Oakland, California, a city known for its diverse culture and burgeoning tech scene. Let's see if this property has house hack potential!

Here’s the duplex we’re looking at - it’s currently listed for $998k and has two 3bd/2ba units.

The home is located in North Oakland, an area known for its residential charm and proximity to both downtown Oakland and Berkeley. The house itself was built in 1911, but looking at the pictures we can see that it was updated recently. We’ll assume that we purchase the property for its asking price of $998k. We won’t allocate any money for immediate repairs and renovations, but since the home is old, we’ll definitely set aside a budget for capex and repairs.

We’re going to make the following assumptions:

20% down with a 30-year fixed mortgage at 7.5% interest rate

1.24% annual property tax rate (based on Oakland’s current rates)

$350/mo home insurance

10% reserve for capex and repairs

5% vacancy rate

2% annual rent and expense increase

Since this is a duplex, we'll live in one unit and rent out the other. Both units are 3bd/2ba, so we'll also rent out two of the bedrooms in our unit for added income.

According to the listing, one of the units is currently rented out for $2,550/mo. If those tenants choose the leave, based on local comps, we’d be able to get around $4,000/mo for the unit. For the bedrooms in our unit, Craigslist suggests we’ll be able to get around $1,000/mo (thanks to the property’s proximity to UC Berkeley). If the current tenants stay, our total monthly rental income will be $4,550. If they leave, it’ll jump to $6,000.

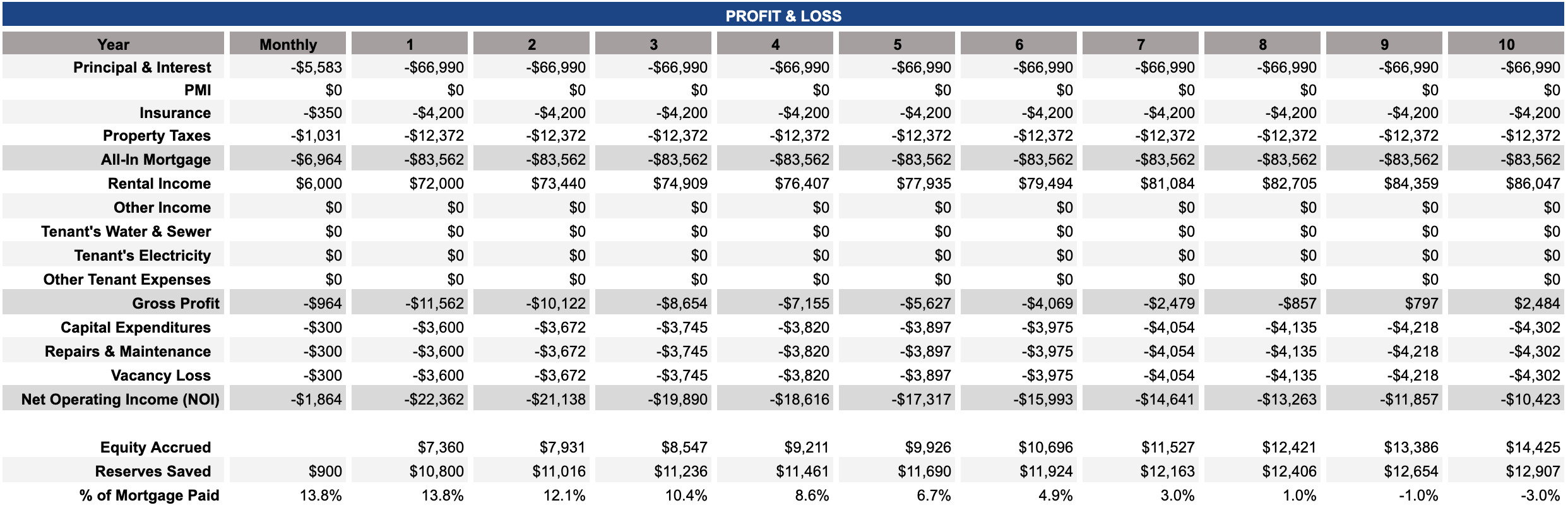

We’ll analyze the bull case where the tenants move out the other unit and we’re able to rent it for $4,000/mo. Plugging these numbers into our house hacking calculator (reply to this email and I’ll send you the link!), we get the results below.

Our monthly outlay for mortgage + insurance + property tax comes out to $6,964 and, in the bull case, we’re bringing in $6,000 in monthly rental income. Subtracting the two, we’re losing $964/mo in our first year living in the property ($11,568 for the whole year). Not off to a good start.

We’re also putting aside $10,800 ($900/mo) in the first year for capex, maintenance, and vacancy. Rolling that into our calculations, our year 1 out-of-pocket living cost comes out to $22,368. We accrue $7,360 in home equity in our first year, so the net living cost comes to $15,008 or $1,250/mo.

Having to shell out $1,250/mo to live in a shared unit in a duplex that you’ve already put 20% down on isn’t great. And don’t forget, this is in the scenario where the other unit comes unoccupied. It’s highly unlikely that the current tenants will move out given their favorable rent.

One strategy to juice our rental income would be to furnish our extra bedrooms and market them specifically for students at Berkeley. The property is close to campus, so it would be highly attractive for students who want to stay nearby. By furnishing the bedrooms, we could expect to make an extra $200-300/mo per bedroom. The extra income would help, but it only reduces our monthly loss by less than half.

Another avenue would be to look into short/medium-term housing. Renting rooms to travel nurses or on Airbnb would probably lead to higher monthly rates compared to long-term leases, but you’d have the additional overhead of more frequent tenant turnover and management.

Would I purchase this property? Probably not. In a market like Oakland, renting often makes more financial sense than buying, especially with current interest rates. On top of that, one of the units is currently rented far below market rate, which seriously limits the property’s income potential in the short-term. You can get creative by offering furnished rooms to students, travel nurses, or Airbnb guests, but none of it seems to be enough to make the property a viable investment.

Thanks for reading! See you next week!